Inflation and the Housing Bubble

Inflation and the Housing Bubble

Generally not a good time to buy a house...

Welcome to another edition of the Mueller Report!

I meant to send this earlier today but I am at a conference and ran out of time between sessions.

I have had a number of conversations over the past week about inflation and housing prices - so I thought I would share a few thoughts, observations, and statistics this week.

What is Inflation?

Milton Friedman once said: “inflation is everywhere and always a monetary phenomenon.” By this he meant that money is an intrinsic part of inflation. He spent most of his career analyzing the growth of the money supply and its effects on the price level.

The basic definition of inflation is the falling value of a currency relative to everything you can buy with it - which manifests itself in generally higher prices across a broad variety of goods, services, or assets.

There is a famous equation called the quantity theory of money to describe the connection between money and prices: MV = Py

It means that the quantity of money (M) * the velocity, or how frequently, it is spent (V) will be equal to all purchases of goods (y) for a given price level (P). A simple thought experiment to illustrate this - first done by Hume and more famously done by Milton Friedman - is to ask what would happen if the amount of money people had magically doubled overnight without any other changes in the economy?

The answer is that prices would double. If MV doubles, then Py doubles. Remember that “y” relates to physical goods that take time and resources to produce - they can’t just be magically created out of thin air (though online services/apps call part of this into question). So a rapid increase in M, not offset by a decline in V, will lead to a rapid increase in prices (P).

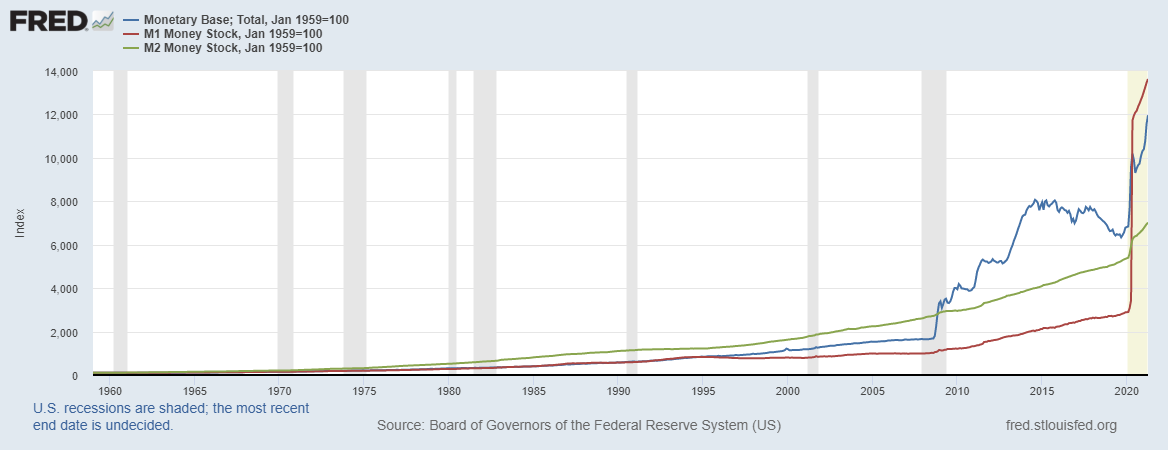

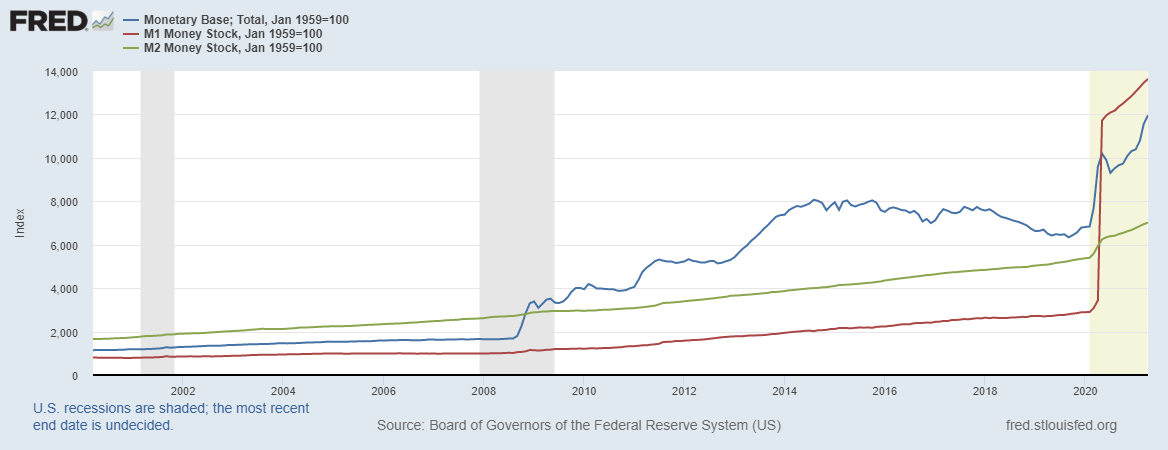

So what has happened to the amount of money in the U. S. recently? There are several measures of money included in the graph below (monetary base, M1, and M2).

As you can see, the fallout from the government response to the 2008 financial crisis led to unprecedented expansion of the monetary base (the blue line). The fiscal shenanigans of Covid stimulus spending has led to an unprecedented increase in M1 (the red line). Has anyone heard of houses being bought with cash recently…?

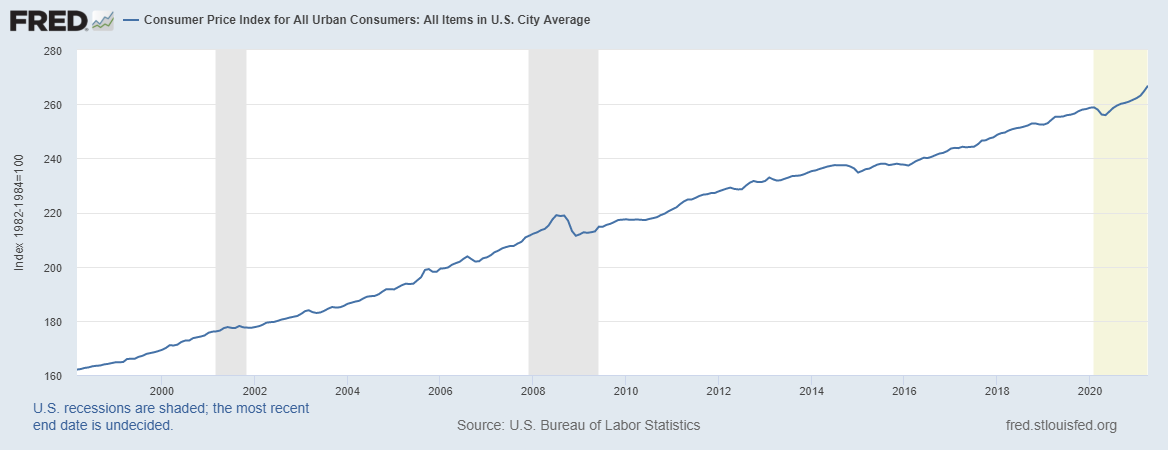

Surprisingly, the traditional measure of inflation, the consumer price index, has increase much less rapidly.

However, the consumer price index generally fails to capture asset-inflation. If increases in the money supply are not primarily spent on goods and services (y), then we would not expect to see P rise very much. Let me give you a sense of the irony here: CPI includes rent costs of housing, but not the price of housing. In NYC right now, rents are falling significantly while house prices are rising…So the “housing” portion of CPI is trending down while the actual cost of houses is trending up.

Perhaps of more interest is a smaller measure of inflation: producer goods and commodities.

You can see a rapid increase in the cost of producer prices of commodities in the past year. This will increase costs of doing business, which will work its way into consumer prices over time.

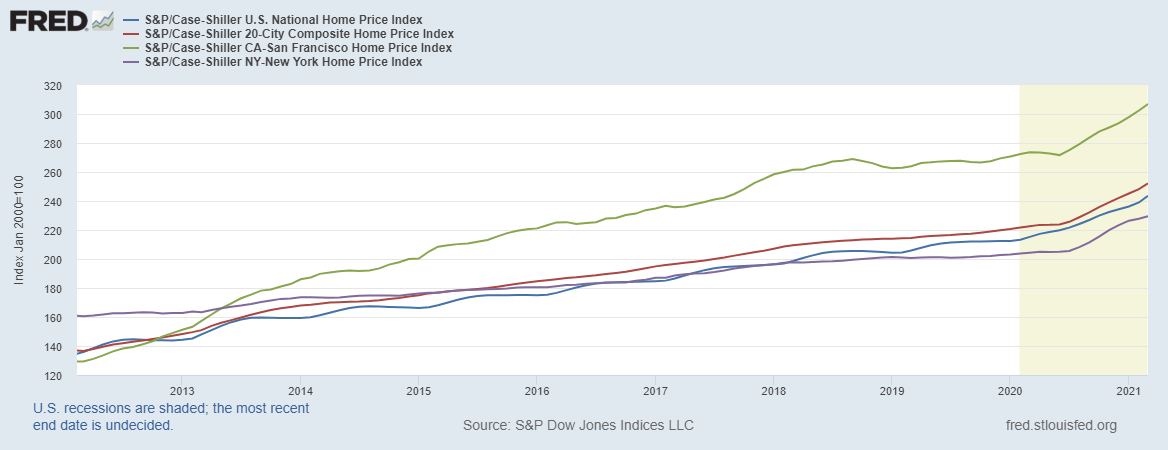

We already see some of its effects in housing prices:

You can see from the graphs of the Case-Shiller index of housing prices above, or from your own experience, that housing prices have been rising rapidly. Notice that housing prices are well above the peak of the housing bubble in 2006 (about 50% higher). We see all the classic indications of a bubble - rapid appreciation of an asset, frenzy to purchase anything and everything that is available, bidding wars above asking price, house flipping, and the like.

The house next to The Abbey sold in one day for at least the asking price - which was itself at least $60,000 than we would have thought reasonable to pay. In our county, the mean price of residential properties sold increased by about 33% over the past year…Many metro areas across the country have seen double digit percentage increases in house prices.

What can’t go on won’t go on.

A ten or more percent annual increase in housing prices is not sustainable because it will outstrip people’s incomes and ability to finance a house purchase, even at rock bottom interest rates. Unless people’s incomes begin to rise commensurately, which could happen if we had widespread consumer price inflation, the rapidly rising housing prices will end sooner rather than later. Just as there is momentum going up, there is momentum going down when people are buying with leverage and speculating on rising prices. A period of painful deleveraging normally follows.

This was the case with Tulips in Holland, this was the case in the 1929 stock crash, the dot com bubble, and the 2007-2008 housing crisis.

I don’t know how all of this will play out or when, but I don’t plan on buying any real estate anytime soon unless is some extreme off-market deal being sold by parties under financial duress.

Talk to you next week!

Paul

Paul,

I enjoyed the Report. Thanks again for doing the research, taking the time to record your thoughts, and put yourself out there (so to speak).

The following sentence resonated with me, "Just as there is momentum going up, there is momentum going down when people are buying with leverage and speculating on rising prices. A period of painful deleveraging normally follows." One of the key phrases you used was, "buying with leverage and speculating." From my vantage point, now is an ideal time to buy a house. However, I would be cautious in buying other real-estate unless you are in a strong financial position to weather short-term vacancies.

Comments on inflation wrt to both your report and Dean Fletcher's response. Inflation is certainly something many are starting to consider given the increase in the money supply. Economic theory it's place and should always be actively discussed and debated. However, theory is just that, theory. Experience is a great teacher. Having lived through the 1970s (and everything since), I vividly remember the impact inflation had on the economy and how it played out in an average person's life. Although, the housing market (and home prices) is "one" measure of the future, I am not convinced it is the best harbinger of what is going to playout in the short-term reference to inflation. I feel Dean Fletcher has a point, but for different reasons. I would avoid putting much stock in Japan's QE actions failing to produce any real inflation given the numerous other factors at play in Japan over the last 30 years. Plus, I am grateful the U.S. has not been living out Japan's economy over the last 30 years. That said, I believe we are "starting" to see the inflationary cycle just beginning. I hope I am proven wrong. However, "hope" is not a method. As I noted above, I believe experience beats theory. I have seen it before (more than once) and am seeing it again now. I am literally placing my money on inflation gaining significant momentum over the next 2-3 years. That said, leveraging the currently interest rates to the degree possible while avoiding significant risk will payoff over the next 5-10+ years. Cheers and Shalom.

You shouldn't only examine the rise in the Monetary base, because the base is expanding due to quantitative easing, or the federal reserve buying assets from banks with federal reserve liabilities. Banks cannot lend out fed liabilities, and they are not "money", and it is not circulating in the general economy where it is needed to contribute to a general and sustained rise in prices. You mentioned Velocity of money, but neglected to discuss how V is at a 6 decade low. https://fred.stlouisfed.org/series/M2V. This matters, and explains why despite 13 years of reserve asset expansion by the central bank, we have yet to see any real Inflation. The federal reserve has only achieved it's stated goal of 2% Inflation for 12 total months over 13 years, despite a 800% increase in assets on their balance sheet via Quantitative easing, creating excess bank reserves, but have reduced the velocity of money by trapping "money" in the commercial banking system, and banks are unable to lend that money in the form of credit expansion. Velocity is key. And when you have hundreds of trillions of dollars in global debt denominated in USD, that debt requires dollars to pay it back, and thus debt based economies are inherently deflationary, or at least disinflationary, as more and more dollars are "destroyed" in order to service larger and larger amounts of USD debt. Also 30 years of bigger and bigger rounds of QE in Japan have failed to produce any real Inflation, same with 4 rounds over 12 years in the USA. I will admit, if the fed can bypass the commercial banking system, create Fed deposit accounts for all Americans, and deposit federal reserve liabilities directly into consumer deposit accounts, we will see high inflation. But absent a change to the Feds charter and the Treasury dept essentially absorbing the federal reserve, we are unlikely to see enough fiscal deficit spending to create a meaningful increase in velocity. MMT isn't getting past the Senate (and I don't think Biden really wants it either).

Don't even get me started on the marginal productivity of debt, and how 150% federal debt to GDP ratios actually creates negative GDP growth, the economy is unlikely to see sustained growth enough to actually create Inflation either.

Moving to housing: when examining housing costs in terms of a monthly payment, instead of nominal prices, we actually see that real housing prices in the US are at near record LOWs. Remember, your average buyer taking out a mortgage isn't concerned about the total price of the home as much as he is affording the monthly payment, and with mortgage interest rates at essentially record lows, the average buyer can now buy a more expensive house at the same monthly payment. In fact, adjusting for interest rates decline and wage growth, homes today are 21% cheaper than they were in 2000. Priced in gold, or cooper, or lumber, or almost any other real asset, housing is very affordable.

https://blog.firstam.com/economics/why-housing-affordability-sank-for-the-first-time-in-over-two-years?utm_campaign=FA%20%7C%20Economics%20Blog%20-%20Monthly%20Round%20Up&utm_medium=email&_hsmi=130984838&_hsenc=p2ANqtz-_Lx0GELkFv5h_6Ev2A61HpOJ5dGRxabb4qgSAIZw5ZAMfDjN2didTKpzATSjt5ovq_YCiX8WqG147-DdCRZiQkEuLGBQ&utm_content=130984838&utm_source=hs_email

So why are housing prices rising to record nominal highs? Basic supply and demand. Millennials are the largest generation ever, and the largest portion of the millennials are now entering peak buying ages (28-35), so demographics are largely driving demand, combined with record low rates Creating this record high home purchasing power. Also, credit worthiness and household balance sheets of perspective buyers have literally never been higher. Americans are flush with cash savings, paying down debt at record levels, and their credit scores are the highest ever. And 2020 saw US incomes rise, despite a recession and record unemployment. This isnt 2005 with a bunch of liar loans and no income, no job, no problem subprime lending. It's the well off leading the way this time. Also consider the surge in second home and investment property purchases, plus the desire for more space post pandemic, WFH long term trends, the suburbanization of buyers... Demand is booming.

On the supply side, there is an estimated shortage of 5 million single family homes in the US. Home builders are only now starting to recover and build new homes at the rates they were in the 90s and early 2000s, so a decade plus of under building has largely contributed it the record low supply of housing. It will take a dozen years of record home building to bridge the supply gap. Additionally, many would be sellers who want to take advantage of their record equity are hesitant to sell because they would be entering into a terrible buyers market, so easier to just stay put, refinance to record low rates, and remodel your house, waiting for the market to moderate.

Some may want to call this a bubble, but unless we see huge secular rise in inflation, causing the fed to drastically raise rates, and thus mortgage rates go into th double digits, we are unlikely to see housing prices decrease for 5-10 years. Powell and his potential replacements will never be Volcker. More likely we see high single digit price appreciation for the near to midterm future.