How to become a millionaire

How to become a millionaire

And an update about the King's intellectual retreat

Welcome to another edition of the Mueller Report!

I meant to get this one out yesterday, but the hotel down the street was getting rid of beds and tables in great condition, so I ended up spending my time picking up and putting together beds and tables. Also, we were sold out last night, which meant more work answering the phone, taking payments, and visiting with people.

Today looks to be similar (there is a bit more to pick up from the hotel and we are sold out again tonight), but I am trying to finish this newsletter first. This week I plan on talking about how to make a million dollars, thoughts on entrepreneurship, and a few highlights from the King’s intellectual retreat we had last week.

How to Get a Million Dollars

Save and invest.

Building wealth fundamentally involves living below your means and investing in projects that bring you some rate of return. I’ve had the opportunity to talk with several recent King’ alumna over the past few weeks who have come out to visit us. In talking about The Millionaire Next Door and Financial Peace, I stressed the advantage they have of being young and how important it is to put together a basic financial plan, even if they are not particularly interested in finance or investing, along the following lines:

Spend less than you make - this will likely involve budgeting.

Set up a Roth IRA account and fund it as much as you can (and are allowed). Not only will the gains be tax free when you retire, you can withdraw your principal anytime you like. In fact, you can also withdraw some of the gains without penalty if it is being used for certain enumerated purchases (college tuition, a house, etc.)

Talk with HR about if your employer provides a retirement matching program - take advantage of it if they do!

Make a plan to buy a house using an FHA loan where you only need to put 3% down. You need to plan on having roommates to offset some or all of your mortgage obligations.

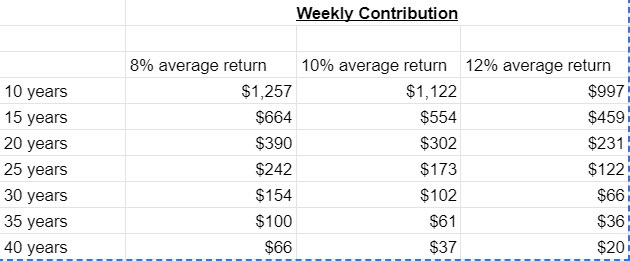

Here is a table of how much money one needs to save and invest in the stock market every week to reach a million dollars in wealth. As you can see, the two variables are time (how long will it take you to become a millionaire?) and rate of return (you don’t have much control over this if you are investing in the general stock market - but the longer your time horizon, the more likely you are to be around the 10% average annual return range.

Assuming a 10% average rate of return, if one of these young ladies saved $302 a week (~$15,600 a year) and invested in the stock market, they would likely have a net worth of a million dollars by the time they are in their early forties. Or only saving $102 a week (~$5300 a year), they could be worth a million dollars by the time they are in their early fifties.

And that is in securities alone. It doesn’t count if they have equity in a house or money in their savings account or if they own a vehicle or two outright.

At an average annual return of 8%, they will have to wait another five years or so to hit a million dollars. At an average annual return of 12%, they will hit a million dollars 2-4 years earlier. The key to the game, though, is diligence and patience. I hope to have my kids start in their late teens. If they save $61 per month (~$3170 per year), they could be worth a million dollars by the time they are in their early forties - and that is not including if they save more or invest additional money in houses or other assets over that time period.

On the flip side, if you want to go from zero (very little net worth) to sixty (a million dollars of net worth) quickly, you have to put in some serious effort. Even at a 12% annual rate of return, you would have to save $997 per week (~$52,000 a year) for ten years. Waiting five more years, or fifteen total, reduces how much you have to save per week by over 50%. If you double the time, from becoming a millionaire in 10 years to becoming one in 20 years, you reduce how much you have to save per week by over a factor of four.

So make a plan if you don’t have one - if not for you, then for your children.

King’s Intellectual Retreat

We had an intellectual retreat for King’s alumni (and a few other guests) last weekend. It was a great time! My hope was for a mix of intentional discussion, informal conversation, and a large amount of relaxation and getting to know one another. I think we hit all three pretty well.

We had several meals together, in which most people lent a hand preparing or cleaning up. We had some time around a fire and most people took a quick jaunt up to the tree line during one of the breaks. An adventurous few went to hike Mt. Sherman, a local 14,000 foot mountain, and took a wrong turn. They ended hiking up a mountain across the valley and then took a long circuit around the bowl to get to the top of Sherman. A four hour hike turned into something like six to seven hours - but they persevered and made it back.

Our formal discussions were structured around a series of articles related to Haidt and Luckianoff’s book The Coddling of the American Mind. I plan on writing a lengthier review of the book elsewhere but here are a couple of the key arguments and a list of the accompanying readings.

Haidt and Luckianoff argue that there are three “great untruths” that are guiding America’s parents, educators, and youth into a dangerous polarization and antagonism towards those they disagree with:

Extreme risk aversion: “What doesn’t kill you makes you weaker. So avoid pain, avoid discomfort, avoid all potentially bad experiences.”

Emotional reasoning: “Always trust your feelings. Never question them.”

Polarization: “Life is a battle between good people and evil people.”

They argue that these three ideas give rise to a variety of modern maladies: depression and anxiety, helicopter or snow blower parenting, trigger warnings and safe spaces, and violence and intolerance of dissent or free speech.

I think all three of these ideas, or at least two and three, grow directly out of cultural Marxism and mid to late 20th century deconstructionism - but I’ll save those thoughts for a different outlet. Here is the list of readings for the retreat:

Session I

Haidt & Luckianoff, “The Coddling of the American Mind” (Atlantic Essay)

Session II

Haidt & Skenazy, “The Fragile Generation” (Reason Essay)

Twenge, “Have Smartphones Destroyed a Generation?” (Atlantic Essay)

Session III

Haidt & Luckianoff, “Three Great Untruths That Are Harming Young Americans” (Book Excerpt on Heleo)

Session IV

Brooks, “The Age of Coddling is Over” (NYT Article)

Douthat, “The Age of Decadence” (NYT Article)

Haidt & Luckianoff, “How to play our way to a better democracy” (NYT Article)

We hope to have several intellectual retreats in 2022. I’ll announce those when we make a schedule, so stay tuned!

Entrepreneurship and Wealth

As you know, I’ve been reading several books about building wealth and having many conversations with folks about the ideas in those books. I’ve written brief reviews of The Millionaire Next Door and Financial Peace already. I hope to have a review of Retire Young, Retire Rich completed in the next week or two. Here are a few general themes in those books that I develop in my reviews:

Building wealth is directly related to one’s lifestyle, especially the habits of frugality, contentment, and investment

You are much less likely to become wealth if you have no goals and if you have no plan or strategy for building wealth

The primary way one builds wealth is through building and/or acquiring assets, whether that is real estate, stocks, or businesses

Mindset is key. How we talk affects how we think and therefore what we do or what we don’t do. Most people do not try to become wealthy because they do not believe they can; which then becomes a self-fulfilling prophecy.

Wage income is an inefficient way of earning money - it requires you to devote a lot of time to earning money since you are paid for your labor, and it tends to be taxed pretty heavily (FICA, disabilities, and income taxes). In contrast, real estate assets, financial assets, and businesses earn you money relatively independently of how much you work at them - they make you money while you sleep!

Next week I will write more about where things stand at The Abbey. We have changed our business model some and we have been working on several minor improvements and projects as we have small chunks of time to do so.

Talk to you next week!

Paul

Enjoyed both the main topic of increasing wealth and the intellectual retreat concept. In addition, I also enjoyed Dean Fletcher's comments.

I concur with your increasing wealth ideas, comments and recommendations. From my vantage point after retiring from two careers and investing since I was 14 years old, I would modify the statement about wage income. I believe a better way to convey or state the idea is that wage income is an inefficient way to "increase wealth" (instead of earning money). Of course, the wage is often the "seed money" that gets the ball rolling (so to speak). As you mentioned, the concept of having your money work for you over an extended period of time are two of the primary components of increasing your financial wealth.

There is also a limit to the amount of wealth you can build by strictly limiting your costs/expenditures. This type of strict frugal living is wise to a certain extent; delayed gratification is great, but don't cut to the point where you are a miserable hermit who doesn't have "fun" or go on vacation. You will only be young once, don't let the prospect of a comfortable retirement in your 50s and beyond ruin the health and energy you have now. It's an individual balance everyone must strike for themselves.

The real wealth creating amplification comes from increasing your income. Change jobs, educate yourself, negotiate on wages, start a side hustle, write an Ebook, buy income generating assets like dividend stocks, rental properties, Airbnb, etc. Multiple income streams, aka diversifying your income beyond just your 9-5, is a safe and risk aware way to maximize the amount you can save and invest for your future.